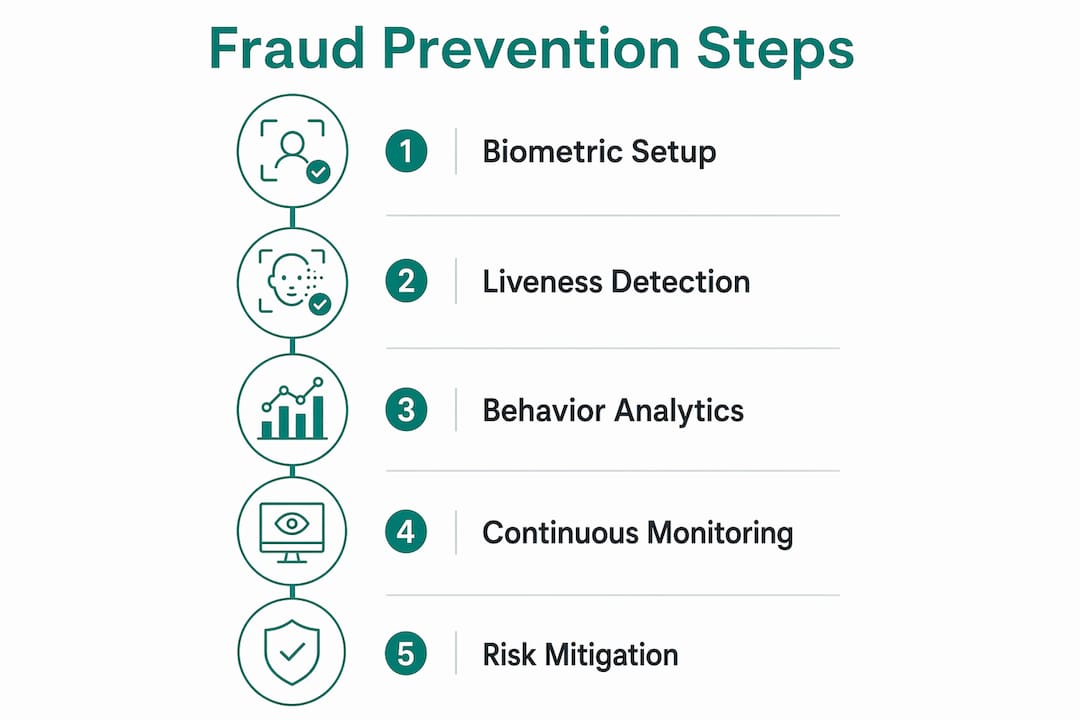

Biometric authentication is defined as identity verification using physical or behavioral characteristics, such as fingerprints, facial geometry, or voice patterns, that are unique to each individual and cannot be transferred or replicated by credential theft. This is the core reason why biometrics reduce bank fraud: they replace shared secrets like passwords and SMS one-time passcodes with device-bound, cryptographic proof of identity. A 2026 deployment at a Tier-1 European bank using Ping Identity’s zero-knowledge biometrics produced a 79% reduction in account takeover fraud and an estimated $2 million in fraud-attempt savings in the first year alone. The FIDO Alliance’s passkey standard and NEC’s trust architecture model both reinforce the same conclusion: biometrics work because they eliminate the attack surface that passwords and SMS OTPs create.

Why biometrics reduce bank fraud at the vector level

Credential theft is the primary entry point for bank fraud. Phishing, SIM swapping, and credential stuffing all depend on one structural weakness: authentication secrets that exist outside the device and can be intercepted, purchased, or socially engineered. Biometrics combined with FIDO2/passkeys remove that weakness entirely.

FIDO2 passkeys are designed to be phishing-resistant by eliminating reusable secrets. The private cryptographic key never leaves the user’s device, so there is nothing for a phishing site to harvest or a SIM swap to redirect. The NCSC confirms that on-device biometric verification as part of cryptographic authentication provides phishing-resistant security equivalent to two-factor authentication, without the SMS interception risk.

The practical impact on account takeover is measurable. The Ping Identity Tier-1 bank case also recorded $4.1 million in helpdesk and SMS cost reductions in the first year. That figure reflects how much of a bank’s operational overhead is tied directly to the fragility of password and OTP systems.

The table below shows where traditional methods fail versus where biometrics hold:

| Authentication method | Primary fraud risk | Biometric advantage |

|---|---|---|

| Password | Credential stuffing, phishing | No reusable secret to steal |

| SMS OTP | SIM swapping, SS7 interception | No out-of-band channel to hijack |

| Email OTP | Account compromise, phishing | No shared secret transmitted |

| FIDO2 passkey + biometric | Device theft (mitigated by liveness) | Cryptographic binding to device and user |

Pro Tip: Audit your current authentication flows for any step that still relies on SMS OTP as a fallback. That single channel is the most commoditized attack vector in retail banking fraud today.

How does liveness detection stop biometric spoofing?

Biometric matching accuracy alone does not determine fraud resistance. A system that correctly matches a face but cannot distinguish a live person from a photograph or a 3D mask is still exploitable. This is why presentation-attack detection (PAD) is the correct evaluation framework, not matching accuracy in isolation.

ISO/IEC 30107-3 is the international benchmark for PAD in biometric systems. NIST guidance aligns with this standard. Banks selecting biometric vendors should require documented PAD test results against ISO/IEC 30107-3, not just vendor-supplied accuracy claims.

The threat landscape has two distinct layers that banks must address separately:

- Presentation attacks at the sensor level: A fraudster presents a fake face, mask, printed photo, or replayed video to the camera. Liveness detection counters this by analyzing micro-movements, texture, depth, or infrared signals.

- Injection attacks in middleware: A fraudster bypasses the sensor entirely by injecting a synthetic or replayed biometric signal into the software pipeline downstream. This attack is invisible to sensor-level liveness controls and requires separate middleware integrity testing.

- Enrollment quality gaps: Poor enrollment, such as low-resolution captures or inconsistent lighting, degrades matching performance and can create false rejection rates that push users toward weaker fallback methods.

- End-to-end trust chain testing: Evaluating a biometric system only at the sensor level misses injection risk. Banks need end-to-end testing that covers the full signal path from capture to decision.

Pro Tip: When evaluating biometric vendors, ask specifically for their injection attack resistance test results. Sensor-level liveness scores tell only half the story.

Does combining biometrics with behavioral analytics improve fraud detection?

Biometric authentication at login is a strong control, but it addresses only the moment of entry. Account takeover fraud increasingly occurs during a session, after a legitimate authentication event. Behavioral analytics fills that gap.

A 2026 Springer Nature review confirms that combining biometric and behavioral signals improves fraud detection capability beyond rule-based systems. The same review advises that governance frameworks covering bias, explainability, and legal compliance are required to deploy these systems responsibly. Detection capability without governance creates legal and reputational exposure.

The integration of behavioral biometrics, covering typing cadence, mouse dynamics, device orientation, and navigation patterns, into an adaptive risk framework works through the following mechanism:

- Baseline establishment: The system builds a behavioral profile for each account holder during normal activity.

- Continuous monitoring: Every session action is scored against the baseline in real time.

- Anomaly triggering: Deviations from normal behavior, such as unusual transaction size, atypical navigation speed, or unfamiliar device posture, trigger a step-up authentication request.

- Biometric step-up: The step-up challenge uses biometric verification rather than SMS OTP, maintaining the phishing-resistant posture throughout the session.

- Adaptive policy adjustment: The system updates the behavioral baseline over time, reducing false positives as user behavior evolves.

This architecture addresses a critical weakness in static rule-based fraud systems. Rules are known quantities that fraud operations test and work around. Behavioral deviation scoring is harder to game because it is specific to each account holder’s actual patterns. Banks that have adopted behavioral fraud detection alongside biometric authentication report fewer false positives and faster fraud detection windows compared to rule-only approaches.

The governance challenge is real. Behavioral biometric models can encode demographic bias if training data is not representative. Explainability requirements under regulations like the EU AI Act mean banks cannot deploy black-box models without audit trails. These are solvable problems, but they require deliberate policy design before deployment, not after.

What implementation pitfalls undermine biometric fraud controls?

The most common failure mode in biometric fraud programs is not technical. It is architectural. Banks deploy strong biometric controls at onboarding and login, then leave account recovery and step-up authentication protected by SMS OTP or knowledge-based questions. Fraudsters know this. They do not attack the strongest point. They find the weakest step in the workflow and exploit it.

NEC’s trust architecture model addresses this directly. Identity assurance sustained during high-risk banking events, including account recovery, beneficiary addition, and large transaction approval, reduces attacker success rates. Biometrics applied only at login create a false sense of security while leaving the most fraud-prone workflows exposed.

The following implementation principles reduce the risk of architectural gaps:

- Eliminate SMS fallback after failed biometric checks. Fallback to weak authentication undermines biometric effectiveness and creates a low-assurance bypass that attackers target deliberately.

- Apply biometric verification at every high-risk event. Onboarding, password reset, beneficiary changes, and high-value transactions all require the same identity assurance level, not just the initial login.

- Use zero-knowledge biometric designs where possible. Ping Identity’s zero-knowledge approach stores no retrievable biometric template. This eliminates the risk of a biometric database breach while meeting privacy compliance requirements simultaneously.

- Audit enrollment quality regularly. Degraded enrollment data increases false rejection rates. Users who cannot authenticate biometrically will request fallback options, recreating the vulnerability the biometric system was meant to close.

- Test the full trust chain, not just the sensor. Injection attacks exploit middleware, not cameras. End-to-end testing must cover every component between capture and decision.

Privacy-preserving biometric designs are not just a compliance checkbox. They reduce fraud risk directly. A retrievable biometric template stored in a central database is a high-value target. Zero-knowledge designs remove that target entirely, which means a database breach cannot yield usable biometric data for replay attacks.

Key takeaways

Biometrics reduce bank fraud most effectively when deployed as a continuous identity assurance layer across all high-risk workflows, not as a single checkpoint at login.

| Point | Details |

|---|---|

| Device-bound authentication eliminates credential theft | FIDO2 passkeys with biometrics remove reusable secrets, blocking phishing and SIM swap attacks. |

| Liveness detection requires PAD evaluation | Assess vendors against ISO/IEC 30107-3 for both sensor-level and injection attack resistance. |

| Behavioral analytics extend protection mid-session | Combining biometrics with behavioral signals detects fraud after login, where static rules fail. |

| Fallback removal is non-negotiable | SMS OTP fallback after failed biometric checks creates a low-assurance bypass attackers exploit. |

| Zero-knowledge designs reduce breach risk | Storing no retrievable biometric template removes the database attack surface while meeting compliance. |

The architecture problem banks keep ignoring

The fraud industry has known for years that SMS OTP is broken. SIM swapping is not a sophisticated attack. It requires a phone call and a social engineering script. Yet a significant share of retail banking authentication flows still route failed biometric checks directly to SMS fallback, which is the exact scenario that passkey adoption was designed to eliminate.

What I find most concerning is not the technical gap. It is the governance gap. Banks invest in biometric sensors and matching engines, then fail to govern the full identity lifecycle. Account recovery remains the most exploited workflow in retail banking fraud, and it is often the least protected. NEC’s framing of biometrics as a trust architecture, rather than a point solution, is the right mental model. Identity assurance is not a feature you switch on at onboarding. It is a property you maintain or lose at every subsequent interaction.

The behavioral analytics layer adds genuine detection capability, but only if the governance framework is built before deployment. Bias in training data, unexplainable model decisions, and legal compliance requirements under frameworks like the EU AI Act are not afterthoughts. They are design constraints. Banks that treat them as such will build systems that hold up under regulatory scrutiny. Banks that do not will face both fraud losses and enforcement action.

The future direction is clear. AI-powered behavioral biometrics, zero-knowledge storage, and FIDO2 passkeys are converging into a single identity assurance stack. Banks that build toward that architecture now will have a structural fraud advantage. Banks that continue patching SMS OTP systems will keep losing ground to fraud operations that have already commoditized the attack.

— Kevin

Fraudsignals: go deeper on biometric fraud prevention

Fraudsignals covers the intersection of identity verification technology and financial fraud with the depth that banking professionals need to make informed decisions.

The biometrics coverage on Fraudsignals tracks developments in liveness detection, zero-knowledge designs, FIDO2 adoption, and behavioral analytics as they apply to banking fraud risk. The identity fraud section covers how continuous biometric verification changes the fraud calculus across the full customer lifecycle. For banking and fintech professionals who need to stay current on authentication standards, regulatory shifts, and real-world deployment outcomes, Fraudsignals publishes research-backed analysis updated as the threat environment evolves. Visit fraudsignals.news to access the full archive.

FAQ

Why do biometrics reduce bank fraud more than passwords?

Biometrics eliminate reusable secrets. Passwords can be phished, purchased, or guessed, while a biometric combined with a FIDO2 passkey is cryptographically bound to the user’s device and cannot be intercepted or replayed.

What is presentation-attack detection in banking biometrics?

Presentation-attack detection (PAD) is the capability to distinguish a live person from a fake biometric sample, such as a photo, mask, or replayed video. ISO/IEC 30107-3 is the international standard banks should use to evaluate PAD performance in biometric vendors.

How does SIM swapping relate to biometric authentication?

SIM swapping hijacks SMS-based authentication by redirecting a victim’s phone number to an attacker-controlled SIM. FIDO2 passkeys with on-device biometrics eliminate this risk because authentication never relies on an out-of-band SMS channel.

What is zero-knowledge biometrics?

Zero-knowledge biometrics is a design approach, used by vendors like Ping Identity, in which no retrievable biometric template is stored. This removes the risk of a database breach yielding usable biometric data and meets strict privacy compliance requirements simultaneously.

Does behavioral biometrics replace traditional biometric authentication?

Behavioral biometrics does not replace traditional biometric authentication. It extends fraud detection into active sessions by monitoring typing cadence, navigation patterns, and device behavior, triggering step-up biometric challenges when anomalies appear.

Recommended

Why Biometrics Satisfy Compliance Requirements in 2026

Top 4 Sources for evssolutions.com alternatives 2026