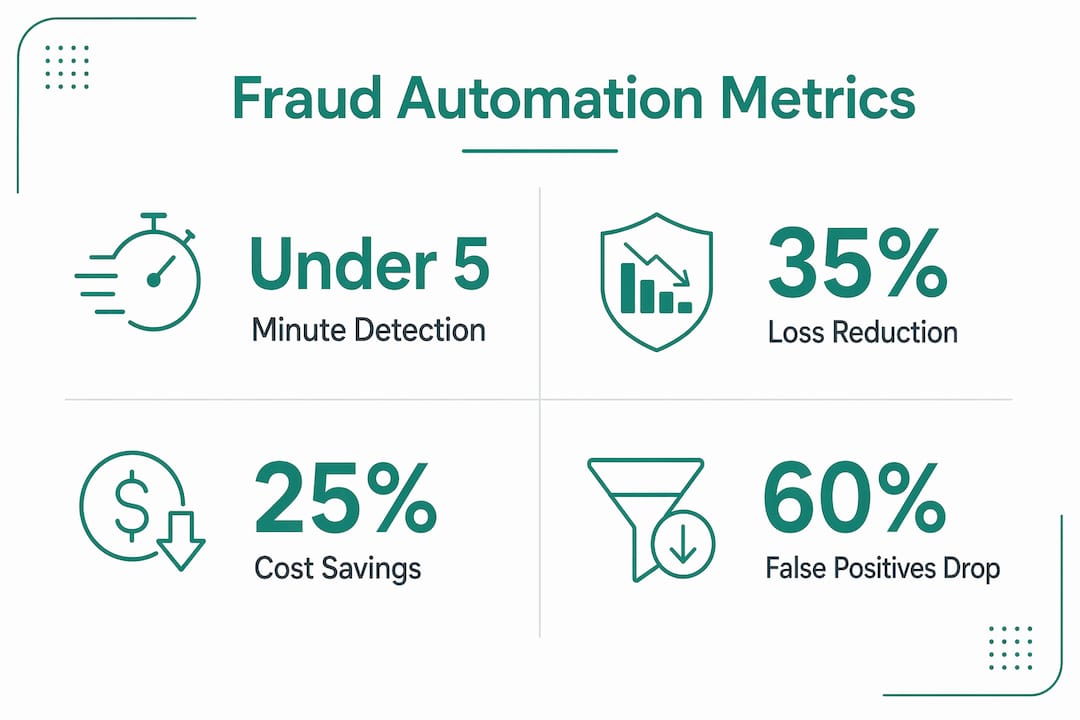

Automation in fraud prevention is defined as the deployment of AI, machine learning, and multi-agent systems to detect, score, and respond to fraudulent transactions in real time, without waiting for human review. Tools like Visa Protect and Mastercard Decision Intelligence now process billions of transactions monthly using this approach. The results are measurable: 67% lower fraud-related costs compared to manual review operations, and detection windows compressed from 72 hours to under five minutes. For fraud prevention professionals managing high-velocity digital transaction environments, understanding the role of automation in fraud prevention is no longer optional. It is the operational baseline.

How does automation speed up fraud detection and response?

Manual fraud review is structurally incapable of matching the speed of modern fraud attacks. A human analyst reviewing a suspicious transaction takes 5–8 minutes on average. Automated pre-scoring and risk analysis cut that window to 1–2 minutes for cases that do reach a human, and eliminates human involvement entirely for the vast majority of transactions.

The most advanced architecture driving this speed is the multi-agent fraud detection system. Rather than routing every transaction through a single large model, these systems decompose fraud detection into specialized agents, each handling a discrete task:

- Identity verification agents cross-reference document data, biometric signals, and device context in parallel.

- Velocity check agents flag abnormal transaction frequency patterns against behavioral baselines.

- Graph analysis agents map relationship networks to surface account takeover rings and synthetic identity clusters.

- Orchestration layers route transactions to the appropriate agent tier based on risk score, avoiding unnecessary computation.

This architecture produces sub-200ms decision latency and costs 15 times less than single-model approaches. The cost differential matters because high-volume merchants process millions of transactions daily. Running every transaction through an expensive large language model evaluation is economically unsustainable. Decomposed agent systems solve this by routing 95% of transactions through low-cost agents, reserving expensive evaluations for genuinely ambiguous cases.

Pro Tip: Treat decision speed as a product feature, not just an operational metric. In real-time payment rails, a 500ms delay is enough to create customer friction and expose a window for fraud to complete. Build your SLA around sub-200ms targets from the start.

How does automation reduce false positives in fraud detection?

False declines are the fraud prevention problem that most institutions underestimate. False declines contribute more financial loss than direct fraud in many merchant categories, because every declined legitimate transaction is lost revenue plus a damaged customer relationship. Static rule-based systems produce high false positive rates because they cannot distinguish context. Automation corrects this through behavioral modeling and graduated response logic.

Here is how AI-powered automation improves accuracy across the detection pipeline:

- Behavioral baseline construction. Machine learning models build individualized profiles for each customer, tracking device fingerprints, transaction timing, geographic patterns, and spending velocity. A transaction that looks suspicious in isolation looks normal when measured against that customer’s established behavior.

- Context-aware scoring. Rather than applying a binary approve or decline decision, automated systems assign a continuous risk score. A score of 0.3 triggers step-up authentication. A score of 0.7 routes to manual review. A score of 0.95 triggers an automatic block. This graduated response model replaces the blunt instrument of static rules.

- Continuous model feedback. AI fraud detection models improve by integrating analyst feedback and evolving transaction patterns in real time, bypassing the typical ML retraining cycles that delay response to new fraud patterns.

- Synthetic identity detection. Continuous behavioral monitoring across the customer lifecycle catches synthetic identities that pass initial KYC checks. Subtle anomalies in activity patterns over weeks or months surface what a one-time verification cannot.

Banks using AI fraud solutions report false positives reduced by 60% and suspicious activity detection increased 2–4 times compared to legacy systems. Automated systems with graduated response logic reduce false declines by 60–75% while maintaining detection rates. That combination, fewer false positives and fewer missed frauds, is the core accuracy argument for automation in fraud detection.

Pro Tip: When tuning your model thresholds, segment by transaction channel and customer cohort separately. A threshold calibrated for card-present transactions will over-block legitimate card-not-present e-commerce orders. One size fits none.

What are the financial and operational benefits of automated fraud prevention?

The return on investment case for automated fraud prevention is concrete and well-documented. Merchants processing 1,000 or more monthly orders achieve positive ROI in 30 days by reducing false declines alone. For enterprise-scale financial institutions, the savings compound across chargebacks, labor costs, and fraud losses simultaneously.

| Metric | Manual review | Automated system |

|---|---|---|

| Detection speed | Up to 72 hours | Under 5 minutes |

| Manual review time per case | 5–8 minutes | 1–2 minutes (enriched cases only) |

| Fraud-to-revenue ratio | 2.5x higher | Baseline |

| Manual review cost | 3x higher | Baseline |

| False positive rate | High (static rules) | Reduced by 60–75% |

| Orders requiring human review | 100% | 2–5% |

| Annual analyst turnover | 35% | Significantly reduced |

The labor dimension is particularly significant. Manual review teams carry 35% annual turnover, which means constant recruitment, onboarding, and training costs on top of the direct review labor. Automated systems handle 95–98% of orders without human involvement. The analysts who remain focus on genuinely complex cases, which improves job quality and reduces burnout.

Banks using AI-driven fraud prevention report fraud losses reduced by 35% and manual review costs lowered by 25%, while processing billions of transactions monthly. The operational math is straightforward: automation scales fraud prevention capacity without adding headcount, which means the cost per transaction reviewed falls as volume grows. Manual operations do the opposite.

What emerging techniques are reshaping fraud automation?

The next generation of fraud automation moves beyond single-model detection toward architectures that mirror how sophisticated fraud rings actually operate. Fraudsters automate their attacks. Effective fraud prevention must automate its defenses at the same level of sophistication.

- Multi-agent architectures with specialized roles. Splitting fraud detection into discrete agents for identity verification, velocity analysis, and graph relationship mapping optimizes both speed and cost. Decomposing fraud detection tasks into specialized AI agents results in sub-200ms decision latency and significant cost savings compared to monolithic models.

- OCR and large language model integration for identity verification. Sun Finance’s deployment on AWS demonstrates the scale of improvement possible. Using OCR combined with large language models for document extraction, processing time dropped from 20 hours to under 5 seconds and accuracy improved from 79.7% to 90.8%. That is not incremental improvement. It is a structural change in what identity verification can accomplish.

- Continuous behavioral monitoring across the customer lifecycle. The Adyen Fraud Report 2026 confirms that fraud tactics evolve rapidly, and static rule sets cannot keep pace. Continuous behavioral baselines detect synthetic identity fraud by spotting subtle anomalies in customer activity over time, catching fraud that passes initial onboarding checks.

- Explainability and compliance integration. PCI-DSS and GDPR both require that automated decisions affecting customers be explainable. Effective fraud automation maintains tamper-proof audit logs and supports human-readable decision rationale for every blocked transaction. This is not optional for regulated financial institutions.

- Federated learning for collaborative intelligence. Federated learning allows institutions to train shared fraud detection models without sharing raw transaction data. This approach improves model accuracy across the industry while preserving data privacy, a critical consideration for cross-border financial services.

Automation is indispensable for scaling fraud prevention precisely because fraud tactics themselves are now automated and adaptive. A fraud ring using credential stuffing bots can probe thousands of accounts per minute. A human analyst cannot respond at that velocity. Only automated systems with real-time behavioral monitoring can.

Key Takeaways

Automated fraud prevention outperforms manual review on every measurable dimension: speed, accuracy, cost, and scale.

| Point | Details |

|---|---|

| Speed advantage | Automated systems detect fraud in under 5 minutes versus up to 72 hours for manual review. |

| False positive reduction | Graduated response models reduce false declines by 60–75% without lowering detection rates. |

| ROI timeline | High-volume merchants achieve positive ROI within 30 days by cutting false declines and chargeback costs. |

| Multi-agent architecture | Decomposed AI agent systems deliver sub-200ms decisions at 15 times lower cost than single-model approaches. |

| Continuous monitoring | Behavioral baselines across the customer lifecycle catch synthetic identities that pass initial KYC checks. |

Why I think most fraud teams are still underestimating automation’s ceiling

I have watched fraud prevention teams invest heavily in automation and still leave significant value on the table. The common failure mode is treating automation as a replacement for static rules rather than as a fundamentally different detection paradigm. Teams port their existing rule logic into an ML model, declare victory, and wonder why performance plateaus.

The real shift happens when you stop thinking about fraud detection as a series of checks and start thinking about it as continuous behavioral intelligence. A transaction is not an isolated event. It is a data point in a customer relationship that spans months or years. The teams getting the most out of automation are the ones building models that treat it that way.

The other underestimated cost is false declines. I have seen fraud teams celebrate low fraud rates while their false decline rate quietly erodes revenue and customer lifetime value. Automation does not just reduce fraud losses. It recovers revenue that static rules were blocking unnecessarily. That is often the larger number, and it rarely shows up in the fraud team’s KPIs.

My practical recommendation: decompose your fraud detection pipeline into discrete tasks before you choose your tooling. Identity verification, velocity analysis, device intelligence, and behavioral scoring each have different latency and cost profiles. Matching the right model architecture to each task is where the real efficiency gains live. Explainability should be built in from the start, not retrofitted when a regulator asks for it.

— Kevin

Stay ahead of fraud automation with Fraudsignals

Fraudsignals covers the automation technologies, identity verification methods, and AI-driven fraud detection strategies that fraud prevention professionals and financial security analysts need to stay current. The platform publishes analysis on multi-agent architectures, behavioral monitoring, synthetic identity detection, and the compliance requirements shaping how financial institutions deploy automated systems. Whether you are evaluating new tooling, tracking emerging fraud tactics, or building the case for automation investment internally, Fraudsignals provides the depth and specificity this work demands. Explore the full resource library to support your fraud prevention strategy.

FAQ

What is the role of automation in fraud prevention?

Automation in fraud prevention uses AI, machine learning, and multi-agent systems to detect and respond to fraudulent transactions in real time. It replaces manual review workflows that cannot match the speed or scale of modern fraud attacks.

How much can automation reduce fraud-related costs?

Businesses using automated fraud detection report 67% lower total fraud-related costs compared to manual review operations. High-volume merchants typically achieve positive ROI within 30 days.

How does automation prevent false positives in fraud detection?

Automated systems build behavioral baselines for each customer and apply graduated risk scoring instead of binary approve or decline decisions. This approach reduces false declines by 60–75% while maintaining fraud detection rates.

What is a multi-agent fraud detection system?

A multi-agent fraud detection system splits fraud analysis into specialized AI agents handling distinct tasks such as identity verification, velocity checks, and graph analysis. This architecture delivers sub-200ms decisions at significantly lower cost than single-model systems.

What compliance requirements apply to automated fraud decisions?

PCI-DSS and GDPR require that automated decisions affecting customers be explainable and auditable. Effective fraud automation maintains tamper-proof audit logs and human-readable decision rationale to satisfy regulatory review.

Recommended

How Digital Identity Wallets Work: A Complete Guide

Top 5 deepidv.com Alternatives for Identity Verification 2026