Digital identity wallets are secure applications that store and manage verifiable digital credentials, giving users direct control over what identity information they share and with whom. Unlike a physical wallet that simply holds cards, a digital identity wallet uses cryptographic technology to prove credential authenticity without exposing unnecessary personal data. Platforms like Apple Wallet and Google Wallet have introduced millions of users to the concept, but the underlying architecture goes far deeper than most realize. Standards from W3C and NIST define how these wallets issue, store, and present credentials across different systems. Understanding how digital identity wallets work is now a practical requirement for any organization operating in fintech, banking, or regulated identity verification.

How digital identity wallets work: the core architecture

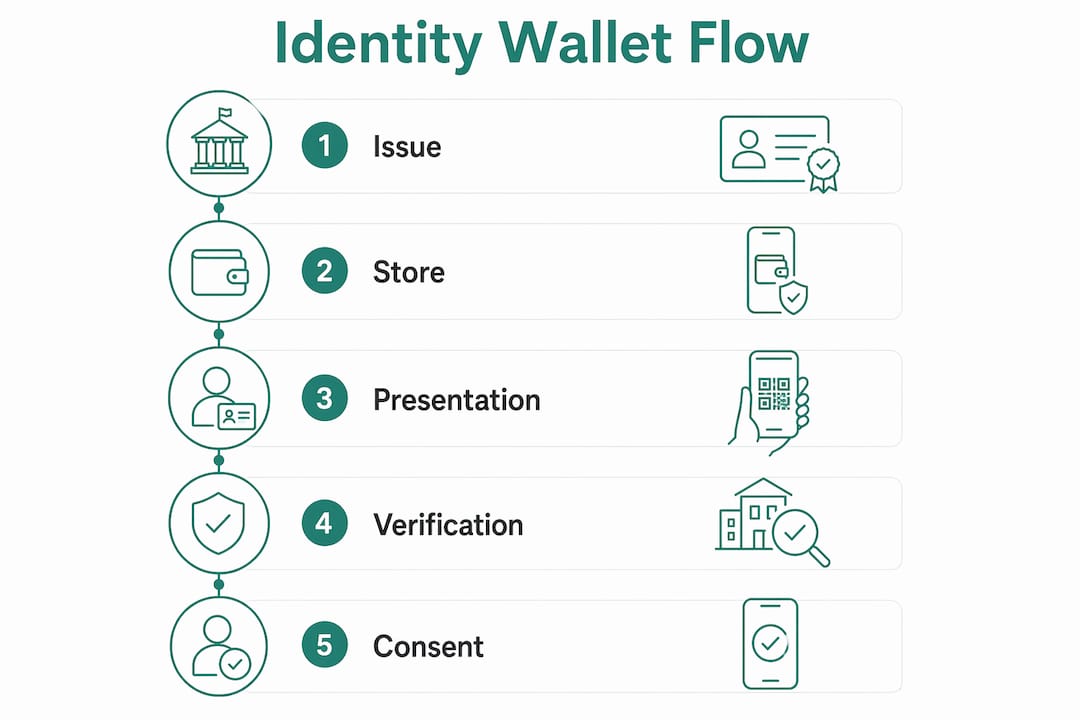

A digital identity wallet operates within a three-party model: an issuer, a holder, and a verifier. Each role is distinct, and the wallet sits at the center as the holder’s controlled presentation layer.

The roles function as follows:

- Issuer: A trusted authority such as a government agency or bank that creates and signs a verifiable credential. A state DMV issuing a mobile driver’s license is a direct example.

- Holder: The individual who receives the credential and stores it in their wallet. The holder controls when and how the credential is presented.

- Verifier: A relying party such as an airline, financial institution, or online service that requests proof of specific attributes and validates the cryptographic signature.

Verifiable credentials are stored in credential repositories (wallets), and holders create verifiable presentations that verifiers cryptographically validate. This means a verifier never needs to contact the issuer directly during a transaction. The cryptographic signature on the credential does the trust work instead.

Issuance follows a standardized protocol. NIST identifies OpenID4VCI as the API protocol for credential issuance, layering atop OAuth 2.0 and OpenID Connect. This means the same authentication infrastructure banks already use can serve as the foundation for issuing verifiable credentials to mobile wallets.

The W3C Digital Credentials specification outlines the presentation protocol in detail, including user agent mediation for wallet selection and consent. The browser or operating system acts as a mediator, ensuring the user actively chooses which wallet responds to a credential request.

Pro Tip: When evaluating wallet platforms for organizational use, confirm that the platform supports OpenID4VCI for issuance and W3C Digital Credentials for presentation. Proprietary protocols create lock-in and break interoperability.

What privacy and security mechanisms protect identity wallets?

Privacy in digital identity wallets is not a feature added on top. It is built into the cryptographic architecture from the ground up.

The four core security mechanisms are:

-

Selective disclosure: The wallet shares only the specific credential fields a verifier requests. A verifier asking for proof of age receives a yes or no answer, not a full date of birth or address. W3C VCALM defines selective disclosure and cryptosuite signaling, including BBS and ecdsa-sd suites, enabling fine-grained disclosure control at the field level.

-

Device key binding: During credential issuance, cryptographic keys are generated on and bound to the holder’s device. NIST identifies device key binding as the security hinge of mobile driver’s licenses and similar credentials. If the credential is extracted from the device, it cannot be used without the private key that stays on the hardware.

-

Encrypted storage: Credentials sit in encrypted storage on the device, accessible only after the user authenticates. Biometric authentication, such as Face ID or fingerprint unlock, gates access to the credential portfolio.

-

Consent mediation: Before any credential data leaves the wallet, the user sees a consent screen. W3C emphasizes that consent UX screens are core to the privacy model, not optional UI polish. The front-end consent screen controls which credential requests get forwarded and which wallets respond.

Selective disclosure is more nuanced than most organizations assume. Its effectiveness depends entirely on credential cryptosuite compatibility and how the verifier structures its request. A poorly formed request can inadvertently trigger disclosure of more fields than intended.

The biggest practical risk is not cryptographic failure. It is poor consent UX design that rushes users through approval screens without clearly communicating what data is being shared. Organizations building verifier integrations must treat the consent interface as a security control, not a formality.

Pro Tip: Test your verifier’s credential request structure against multiple wallet implementations before deployment. A request that works correctly with one wallet may trigger unintended data disclosure with another due to cryptosuite differences.

How do different wallet implementations compare?

Not all digital identity wallets are built the same way, and the differences matter for organizations choosing which platforms to support.

| Dimension | Native platform wallets (Apple, Google) | Third-party wallet apps |

|---|---|---|

| Credential formats supported | Primarily mDL (ISO 18013-5), expanding to W3C VC | Broader format support, varies by vendor |

| Interoperability | Tied to platform ecosystem | Designed for cross-platform use |

| User adoption | High, pre-installed on devices | Requires separate download and onboarding |

| Key recovery | Platform-managed (iCloud Keychain, Google Account) | Vendor-specific, often more complex |

| Standards conformance | Improving, not yet fully standardized | Varies widely; conformance testing required |

NIST describes interoperability efforts across mDL and W3C VC formats as ongoing, with the goal of reducing inconsistency across issuer, holder, and verifier roles. The practical implication is that a verifier today cannot assume a single integration will accept credentials from every wallet a user might have.

Credential format and wallet protocol mechanics are distinct concerns. Interoperability requires conformance beyond UI compatibility. A verifier must be able to accept both mDL-based credentials and W3C Verifiable Credentials to serve a broad user base without forcing users onto a single platform.

Device migration is a real operational challenge. Because credentials are cryptographically bound to a specific device, moving to a new phone requires re-issuance of credentials rather than a simple data transfer. Organizations issuing credentials must build re-issuance workflows into their identity lifecycle management from the start.

What are the practical uses and benefits of digital identity wallets?

The benefits of digital identity wallets extend well beyond convenience. They change the fundamental economics of identity verification for organizations and reduce fraud exposure at the same time.

Key use cases include:

- Mobile driver’s licenses (mDL): Several U.S. states now issue mDLs accepted at TSA checkpoints and select retailers. The credential is cryptographically signed by the DMV, making forgery computationally infeasible.

- KYC and onboarding: Financial institutions can request a verifiable credential for KYC verification instead of collecting raw document scans. The wallet presents a cryptographic proof that the issuer verified the user’s identity, without the bank ever storing a copy of the passport or driver’s license.

- Electronic signatures: A wallet holding a signing certificate can execute legally binding digital signatures tied to a verified identity, replacing wet signatures in many regulated workflows.

- Age and eligibility verification: Retailers and online platforms can verify age or professional credentials without collecting any personally identifiable information beyond the specific attribute requested.

For organizations, the fraud prevention angle is direct. Wallet-based identity verification eliminates the document fraud vector entirely. A fraudster cannot submit a forged document when the verifier is checking a cryptographic signature from a trusted issuer rather than inspecting an image file.

The World Bank’s digital ID framework highlights that decentralized architectures distributing trust among issuers and verifiers reduce dependence on any single central authority. This matters for resilience. No single breach point can compromise the entire identity ecosystem.

The future outlook is clear. Adoption is accelerating as standards mature and governments issue more credentials in wallet-compatible formats. Organizations that build verifier infrastructure now will be positioned to accept a growing range of government and institutional credentials without rebuilding their identity stack.

Key Takeaways

Digital identity wallets eliminate document fraud by replacing raw credential inspection with cryptographic proof from trusted issuers, making forgery computationally infeasible across the issuer, holder, and verifier model.

| Point | Details |

|---|---|

| Three-party trust model | Issuers sign credentials, holders store them, and verifiers validate cryptographic proofs without contacting the issuer. |

| Selective disclosure is technical | BBS and ecdsa-sd cryptosuites enable field-level disclosure control, but verifier request structure determines actual data exposure. |

| Device binding is the security hinge | Cryptographic keys bound to the holder’s device make extracted credentials unusable, but require re-issuance workflows on device migration. |

| Consent UX is a security control | W3C treats consent screens as core privacy enforcement, not optional UI. Poor design creates real data leakage risk. |

| Interoperability is still maturing | Supporting both mDL and W3C VC formats is required to serve users across Apple, Google, and third-party wallet platforms. |

Why the consent layer deserves more attention than it gets

The technical community spends considerable energy debating cryptographic suites and protocol conformance. The consent layer gets far less scrutiny, and that is a mistake.

From my perspective, the most underestimated risk in digital identity wallet deployments is not a cryptographic weakness. It is a poorly designed consent screen that a user taps through in two seconds without reading. The privacy model that W3C and NIST have built is genuinely strong. But it assumes the user understands what they are approving. When the consent UX is designed to minimize friction rather than maximize comprehension, the privacy guarantee collapses at the human layer even while the cryptography holds.

Organizations deploying verifier integrations in fintech and banking tend to focus on the backend: protocol conformance, credential format support, revocation checking. These matter. But the front-end consent interface is where the privacy model either holds or fails in practice. A user who does not understand that they are sharing their full address when they intended to share only their age has been failed by the system, regardless of how correct the cryptography is.

The other issue that rarely gets discussed is recovery. Device key binding is the right security architecture. But most organizations issuing credentials have not built re-issuance workflows that are fast and friction-free. When a user loses their phone, they should be able to re-issue their credentials in minutes, not days. Until that operational reality matches the cryptographic promise, wallet adoption will stall among users who have experienced a device loss.

Watch for two developments in the near term: broader government mDL issuance across U.S. states, and W3C Digital Credentials reaching full recommendation status. Both will accelerate the ecosystem significantly.

— Kevin

Fraudsignals covers the identity verification topics that matter

Digital identity wallets represent one piece of a larger identity verification picture. The fraud vectors that wallets address, including document forgery, synthetic identity, and KYC bypass, connect directly to the broader fraud prevention challenges that financial institutions face every day.

Fraudsignals tracks the intersection of identity technology and financial fraud across banking, fintech, and regulated industries. The site covers AI-driven fraud detection, biometric authentication, KYC compliance, and the emerging credential standards reshaping how organizations verify who they are dealing with. For organizations building or upgrading identity verification infrastructure, Fraudsignals provides the technical depth and fraud context that generic technology coverage misses.

FAQ

What is a digital identity wallet?

A digital identity wallet is a secure application that stores verifiable digital credentials and allows users to selectively share identity attributes with verifiers using cryptographic proofs. Examples include mobile driver’s licenses stored in Apple Wallet or Google Wallet.

How does selective disclosure work in identity wallets?

Selective disclosure uses cryptographic suites such as BBS or ecdsa-sd to let a holder share only specific credential fields, for example proof of age, without revealing the full credential. The W3C VCALM specification defines how this field-level control is implemented.

Are digital identity wallets secure against fraud?

Yes, because credentials are cryptographically signed by trusted issuers and bound to the holder’s device. A verifier checks the cryptographic signature rather than inspecting a document image, which eliminates the document forgery vector that criminals exploit in traditional KYC processes.

What is the difference between mDL and W3C Verifiable Credentials?

An mDL (mobile driver’s license) follows the ISO 18013-5 standard and is primarily used for government-issued identity documents. W3C Verifiable Credentials is a broader format supporting a wider range of credential types. NIST notes that interoperability between these formats is an active area of standardization work.

What happens to wallet credentials when you get a new phone?

Because credentials are cryptographically bound to the original device’s keys, they cannot simply be transferred. The holder must request re-issuance of each credential from the original issuer. Organizations issuing credentials should build fast re-issuance workflows to prevent this from becoming a significant friction point.

Recommended

Top 5 deepidv.com Alternatives for Identity Verification 2026

Automation's Role in Fraud Prevention: 2026 Guide