Biometrics satisfy compliance requirements by generating verifiable, auditable identity evidence that static credentials cannot produce. Unlike passwords or PINs, a biometric match ties an authentication event to a specific individual at a specific moment, creating the kind of irrefutable proof that regulators demand. Standards including NIST SP 800-63-4, PCI DSS, SOC 2, and ISO 27001 all require high-assurance identity controls, and biometric systems address those requirements directly. For compliance officers and risk managers in financial institutions, understanding why biometrics satisfy compliance requirements is no longer optional. It is a prerequisite for building defensible identity governance programs in 2026.

Why biometrics satisfy compliance requirements across major frameworks

Biometrics align with regulatory frameworks because they produce timestamped, individual-linked access records that manual processes consistently fail to generate. Audit-ready access logs tied to unique individuals eliminate the reconciliation failures that plague shared credential environments under SOC 2, ISO 27001, and PCI DSS reviews. That specificity is what separates biometric authentication from every other control category.

NIST SP 800-63-4 mandates biometrics and liveness detection for high-assurance identity workflows, particularly at Authentication Assurance Level 2 (AAL2) and paired with hardware authenticators at AAL3. AAL3 is the federal benchmark for privileged access and high-value transaction authorization. Financial institutions operating under federal oversight cannot meet that benchmark with knowledge-based authentication alone.

KYC and AML mandates from regulators including FinCEN require high-assurance identity proofing at onboarding. Biometric verification at Identity Assurance Level 3 (IAL3) satisfies that requirement by confirming that the person presenting credentials is physically present and matches a trusted identity document. That confirmation is what KYC programs are built to achieve.

Pro Tip: Map each biometric control you deploy to a specific regulatory clause, such as NIST AAL2 or PCI DSS Requirement 8.3, before your next audit cycle. Auditors respond to direct control-to-requirement traceability, not general technology descriptions.

The role of biometric MFA in Strong Customer Authentication (SCA) under PSD2 is equally direct. On-device biometric storage satisfies SCA by reducing data exposure while meeting both PSD2 and GDPR requirements at the same time. That dual compliance benefit is one of the clearest advantages of biometric systems over server-side credential storage.

Key regulatory frameworks and the biometric controls they require:

- NIST SP 800-63-4: Liveness detection and biometric binding at AAL2 and AAL3

- PCI DSS Requirement 8.3: Multi-factor authentication for all non-consumer accounts

- SOC 2 Type II: Continuous access control evidence with individual attribution

- ISO 27001 Annex A.9: Access control policy enforcement with audit trail integrity

- KYC/AML (FinCEN): High-assurance identity proofing at onboarding and re-verification

- PSD2 SCA: Possession plus inherence factors, satisfied by on-device biometric MFA

Privacy and data governance in biometric compliance

Privacy law is the most complex layer of biometric compliance, and it is where implementations most often fail. GDPR, the Illinois Biometric Information Privacy Act (BIPA), and the California Consumer Privacy Act (CCPA) each impose specific obligations on how biometric data is collected, stored, and deleted. Treating these laws as a single unified framework is a mistake. Each has distinct consent, retention, and breach notification requirements.

Compliant biometric implementations follow these data governance steps:

- Establish lawful basis before collection. GDPR requires explicit consent or a documented legitimate interest for biometric data processing. BIPA requires written consent and a published retention schedule before any collection occurs.

- Apply purpose limitation. Purpose limitation and data minimization principles prohibit using biometric data collected for authentication to serve secondary purposes such as behavioral analytics or marketing profiling.

- Store irreversible templates, not raw images. Raw facial images or fingerprint scans carry far greater regulatory risk than one-way mathematical templates. Storing templates instead of images reduces the data minimization burden under GDPR and CCPA.

- Conduct a Data Protection Impact Assessment (DPIA). GDPR Article 35 requires a DPIA before deploying any high-risk processing technology, and biometrics qualify by definition. A DPIA documents the risk, the mitigation, and the residual exposure.

- Define and enforce a data lifecycle policy. Consent withdrawal, employee termination, and account closure must each trigger a documented deletion process. Regulators audit deletion records, not just collection records.

Pro Tip: Use cancelable biometric templates that are non-invertible. If a template is compromised, you can revoke and reissue it without exposing the underlying biometric. That capability simplifies breach notification under both GDPR and BIPA significantly.

North American institutions face a layered regulatory environment that compounds these obligations. Multi-jurisdictional compliance readiness requires automated, audit-ready record retention and privacy-first biometric architectures to address state and federal laws simultaneously. Illinois, Texas, Washington, and New York each have active or pending biometric privacy statutes, and federal legislation continues to advance.

Common audit pitfalls in biometric compliance operations

Biometric compliance fails most often not at deployment, but during ongoing operations. The technology works. The governance around it does not keep pace.

The most common audit failures compliance officers encounter:

- Mismatch between biometric matching and identity governance. A biometric match confirms that the person is who they claim to be. It does not confirm that the person is authorized to perform the requested action. Access policy governance must sit on top of biometric authentication, not be replaced by it.

- Immature liveness detection. ISO/IEC 30107-3 is the standard for biometric presentation attack detection. Systems that lack mature liveness detection fail against high-resolution print attacks and digital replay attacks. Auditors increasingly ask for ISO/IEC 30107-3 conformance evidence.

- Treating biometric templates as equivalent to passwords. They are not equivalent. Biometric match results are probabilistic, not binary. A false acceptance rate above the threshold defined in your security policy is a control failure, not a system quirk.

- Neglecting exception handling and override paths. Every biometric system has fallback authentication paths for users who cannot complete biometric verification. Those paths carry the same compliance obligations as the primary path. Auditors examine override logs specifically because they are a common low-assurance bypass.

- Compliance drift between audit cycles. Recurring audits every 6–12 months verifying unauthorized collection prevention and retention policy enforcement are the operational standard. Institutions that audit only at deployment consistently fail their second regulatory review.

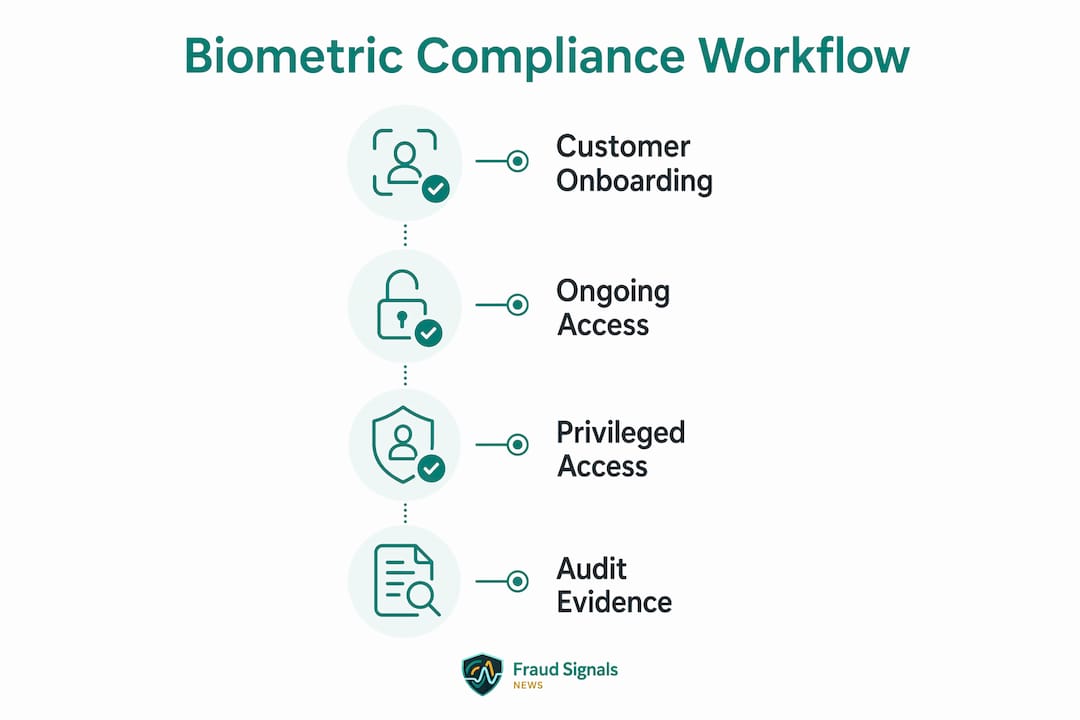

Practical biometric applications in regulated financial institutions

Financial institutions apply biometrics across three primary compliance-relevant workflows: customer onboarding, ongoing authentication, and privileged access control. Each workflow carries distinct regulatory obligations and produces distinct audit evidence.

At onboarding, IAL3-certified biometric verification confirms physical presence and document authenticity simultaneously. That confirmation satisfies FinCEN’s Customer Identification Program requirements and produces a timestamped enrollment record that regulators can examine. The enrollment event log becomes part of the institution’s KYC file, not a separate technology record.

For ongoing account access, biometric MFA with on-device storage meets PSD2 SCA requirements while keeping sensitive biometric data off centralized servers. That architecture reduces GDPR exposure because the institution never processes the raw biometric. The device processes it locally and returns only a pass or fail signal.

Privileged access control for system administrators and treasury operators requires AAL3 controls under NIST SP 800-63-4. Biometric authentication paired with a hardware security key satisfies that requirement. The combination produces an access log that names the individual, the device, the time, and the outcome. That log satisfies SOC 2 Type II continuous monitoring requirements without additional manual reconciliation.

| Workflow | Regulatory requirement | Biometric control | Audit evidence produced |

|---|---|---|---|

| Customer onboarding | FinCEN CIP, KYC/AML | IAL3 biometric verification | Timestamped enrollment record |

| Account authentication | PSD2 SCA, PCI DSS 8.3 | On-device biometric MFA | Per-session authentication log |

| Privileged access | NIST AAL3, SOC 2 | Biometric plus hardware key | Individual-attributed access record |

| Employee offboarding | GDPR, BIPA deletion | Template revocation | Deletion confirmation record |

Compliance officers managing KYC and AML programs benefit directly from automated record retention tied to biometric events. OFAC screening and FinCEN suspicious activity reporting both require documented identity evidence. Biometric enrollment records satisfy that documentation requirement without manual data entry or reconciliation.

Key Takeaways

Biometrics satisfy compliance requirements because they produce individual-attributed, timestamped identity evidence that aligns directly with NIST SP 800-63-4, PCI DSS, SOC 2, ISO 27001, and KYC/AML mandates.

| Point | Details |

|---|---|

| Regulatory framework alignment | Biometrics meet NIST AAL2/AAL3, PCI DSS 8.3, and KYC/AML requirements through verifiable identity linkage. |

| Privacy law obligations | GDPR, BIPA, and CCPA require consent, purpose limitation, and irreversible template storage before deployment. |

| Cancelable templates reduce breach risk | Non-invertible templates can be revoked and reissued, simplifying breach response under GDPR and BIPA. |

| Operational audits prevent compliance drift | Audits every 6–12 months on data retention and collection policies maintain ongoing compliance integrity. |

| Governance beyond authentication | Access policy, exception handling, and deletion records must accompany biometric controls to pass regulatory review. |

The governance gap that technology alone cannot close

Compliance officers who treat biometric deployment as a compliance checkbox will fail their next audit. I have seen this pattern repeatedly. An institution deploys a well-configured facial recognition system, passes its initial SOC 2 review, and then lets the governance layer atrophy. Eighteen months later, the override logs are unreviewed, the deletion records are incomplete, and the liveness detection version has not been updated since deployment.

The technology is not the problem. Biometrics are genuinely the most defensible identity control available to financial institutions right now. The problem is that compliance programs built around biometrics require the same operational discipline as any other control category. Consent records expire. Employees leave. Jurisdictions add new statutes. The biometric system keeps working, but the compliance posture quietly degrades.

The institutions that get this right treat biometric compliance as a continuous process, not a deployment milestone. They run lightweight internal audits on a defined schedule. They maintain a living data lifecycle policy. They test their exception handling paths with the same rigor they apply to the primary authentication path. That discipline is what separates a defensible compliance program from a technology investment that creates liability.

The regulatory direction is clear. NIST SP 800-63-4, PSD2, and emerging federal biometric privacy legislation all point toward higher assurance requirements and stricter data governance. Institutions that build governance infrastructure now will adapt to those requirements without crisis. Institutions that do not will face the same remediation cycle that credential-based programs have been running for a decade.

— A. Johnson

Biometric compliance intelligence from Fraud Signals News

Staying current on biometric compliance means tracking regulatory updates, liveness detection standards, and identity governance developments as they happen.

Fraud Signals News covers the full spectrum of biometric compliance developments, from NIST SP 800-63-4 implementation guidance to ISO/IEC 30107-3 audit requirements and emerging state biometric privacy statutes. The research coverage includes automated record retention practices, audit-ready documentation frameworks, and identity fraud risk analysis built specifically for compliance professionals in financial services. For compliance officers and risk managers who need to stay ahead of regulatory change without filtering through vendor marketing, Fraud Signals News delivers the signal without the noise.

FAQ

Why do biometrics satisfy compliance requirements better than passwords?

Biometrics produce individual-attributed, timestamped authentication records that passwords cannot generate. Regulators including NIST and PCI DSS require that level of identity assurance for high-risk access controls.

What is NIST SP 800-63-4 and how does it apply to biometrics?

NIST SP 800-63-4 is the federal digital identity guideline that mandates liveness detection and biometric binding at AAL2 and AAL3. Financial institutions under federal oversight use it as the baseline for authentication assurance levels.

How do GDPR and BIPA affect biometric compliance in financial institutions?

GDPR requires explicit consent, purpose limitation, and a DPIA before biometric processing. BIPA requires written consent and a published retention schedule. Both laws mandate documented deletion processes when consent is withdrawn or employment ends.

What is a cancelable biometric template?

A cancelable biometric template is a non-invertible mathematical representation of a biometric that can be revoked and reissued if compromised. It reduces breach notification obligations under GDPR and BIPA because the underlying biometric cannot be reconstructed from the template.

How often should financial institutions audit their biometric compliance programs?

Recurring audits every 6–12 months are the operational standard for verifying data retention policies, unauthorized collection prevention, and exception handling integrity. Institutions that audit only at deployment consistently fail subsequent regulatory reviews.

Recommended

Top 4 Sources for evssolutions.com alternatives 2026