Authorized Push Payment (APP) fraud is defined as a scam where a victim is manipulated into willingly transferring funds to an account controlled by a fraudster. Implementing the right push payment fraud prevention steps is not optional for financial institutions and businesses. It is a regulatory and operational necessity. The UK’s mandatory APP reimbursement framework, active from October 2024, caps eligible claims at £85,000 and splits costs 50/50 between sending and receiving payment service providers. That financial exposure alone forces institutions to treat prevention as a core business function, not a compliance checkbox.

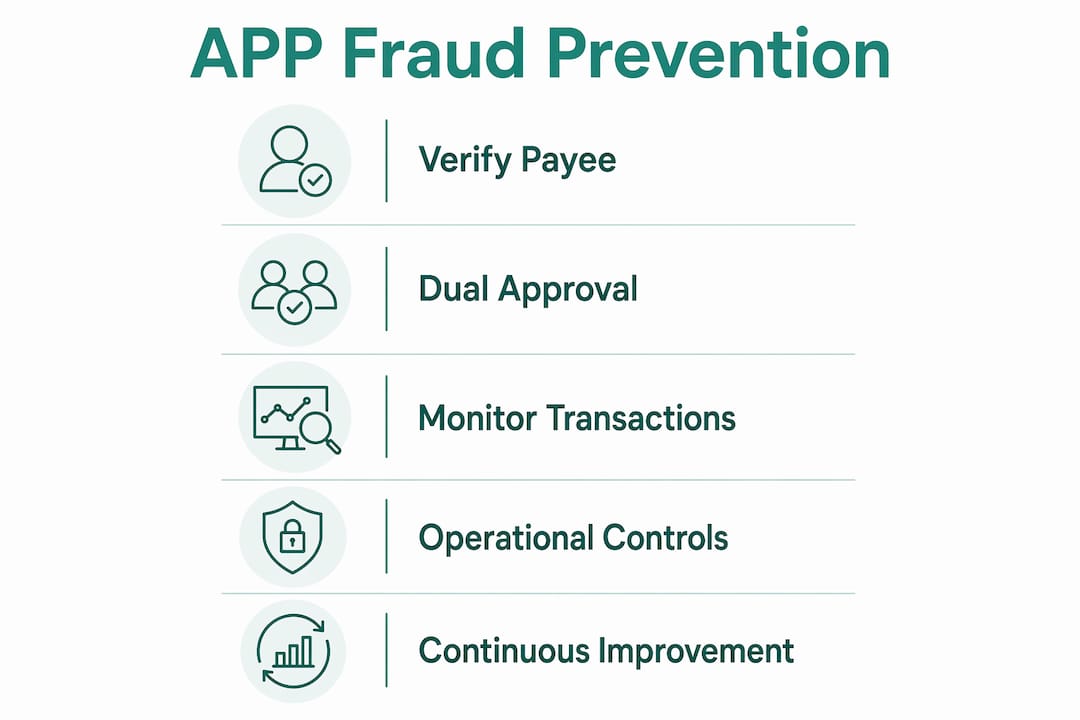

What are the core push payment fraud prevention steps?

Every financial organization needs a layered set of controls. No single measure stops APP fraud on its own. The following steps form the foundation of any credible defense.

-

Implement Confirmation of Payee (CoP) or Verification of Payee (VoP). These systems validate recipient account details before a payment is authorized. CoP mismatch results are classified as match, close match, or no match. Each outcome triggers a specific, actionable message that allows the payer to correct or cancel the transaction before funds leave the account.

-

Deploy layered multi-factor authentication (MFA). MFA on payment portals and employee email accounts blocks a significant share of Business Email Compromise (BEC) routes. Securing email via MFA is critical to blocking upstream scams that target payment systems. Behavioral biometrics, which analyze typing patterns and device interaction, add a further layer that is difficult to spoof.

-

Require dual approval for high-value payments. Dual approval and dollar thresholds limit the risk from any single individual initiating a fraudulent transfer. Set specific dollar limits that trigger mandatory secondary sign-off from an authorized executive or a separate team member.

-

Establish out-of-band verification for payment instruction changes. When a supplier sends new bank details or an urgent payment request arrives by email, do not act on it without independent confirmation. The “pause, stop, look, call” approach directs staff to verify through a trusted phone number already on file, not one provided in the suspicious message.

-

Set transaction monitoring thresholds. Define normal payment patterns for each account or business unit. Transactions that deviate from those patterns in amount, frequency, or destination should trigger automated review before processing.

-

Run regular fraud-awareness training. Staff who recognize social engineering tactics, invoice fraud, and impersonation scams are a genuine control layer. Training should include scenario-based exercises, not just annual policy readings.

Pro Tip: When setting dual approval thresholds, calibrate them to your actual payment data. A threshold set too high covers only a fraction of real fraud attempts. Review your transaction history and set the limit at the point where unusual payments actually cluster.

How can businesses design verification workflows that avoid warning fatigue?

Warning fatigue is one of the most underestimated failure modes in push payment security. When users see too many alerts, or alerts that are too vague, they learn to click through without reading. The result is that a genuine fraud warning gets ignored at the exact moment it matters most.

Effective push payment fraud prevention requires blending technology with well-designed human workflows to minimize alert fatigue and maximize user compliance. The design principles below translate that insight into operational practice.

-

Trigger verification only at meaningful risk points. Not every payment needs an interruption. Risk-based triggering reserves friction for first-time payees, large transfers, and accounts flagged by behavioral anomalies. Routine payments to established, verified payees should process without interruption.

-

Use specific, tiered outcome messages. A message that says “name does not match account records” is more useful than a generic “payment warning.” Tiered outcomes such as soft warnings, hard stops, and step-up reviews give users clear direction and give your team a proportionate response to each risk level.

-

Log every override. When a user proceeds past a warning, that event should be recorded with a timestamp, the specific mismatch type, and the payment details. Analyzing override patterns reveals which alerts users ignore most, which tells you where your messaging is failing.

-

Replace generic banners with precise guidance. “Are you sure you want to proceed?” is not a fraud control. It is noise. Replace it with language that names the specific discrepancy and tells the user exactly what to do next.

“Frequent or vague prompts cause users to ignore alerts, reducing fraud control effectiveness.” This is not a user behavior problem. It is a design problem. Institutions that treat alert fatigue as a workflow engineering challenge, rather than a user education problem, consistently achieve better fraud detection rates.

What operational controls reduce APP fraud risk beyond technology?

Technology controls fail when the underlying business processes are weak. The following operational procedures close the gaps that fraudsters exploit when they cannot defeat the technical layer directly.

-

Enforce strict supplier onboarding and periodic re-verification. Every new supplier should go through a documented onboarding process that confirms bank account ownership. Re-verification should occur on a scheduled cycle and whenever account details change.

-

Prohibit bank detail changes via email. This single rule eliminates a large category of invoice fraud. Require signed documentation on company letterhead and verbal confirmation through a pre-registered contact number before any bank detail change is processed.

-

Segregate duties across procurement, payment initiation, and bookkeeping. No single employee should be able to add a new payee and authorize a payment to that payee. Three-way matching, which reconciles purchase orders, delivery receipts, and invoices, catches discrepancies before payment is released.

-

Apply MFA to all executive and finance team email accounts. BEC attacks frequently target CFOs and finance directors. A compromised executive email account can authorize fraudulent payments that bypass every other control. MFA is the minimum standard here.

-

Develop a written incident response plan. When a suspected fraud event occurs, staff need a clear escalation path. The plan should name specific contacts, define response timelines, and include steps to freeze or recall payments where possible.

-

Use backchannels for urgent or unusual payment requests. Phone or video verification through independent, trusted channels prevents fraudsters from exploiting spoofed contact details embedded in fraudulent messages.

Pro Tip: Build your backchannel contact list proactively. Collect verified phone numbers for all key suppliers and internal approvers before a fraud attempt occurs. Trying to find a trusted contact number during an active incident wastes critical response time.

How do you monitor and continuously improve your fraud defenses?

Controls that are not measured degrade over time. Fraudsters adapt their tactics, and a prevention framework that was effective twelve months ago may have exploitable gaps today. Continuous monitoring and periodic review are what separate a static policy document from a functioning fraud defense.

AI-led transaction monitoring with behavioral biometrics improves real-time fraud detection beyond what traditional rule-based systems can achieve. These systems build behavioral profiles for each account and flag deviations that a static rule set would miss entirely.

The table below outlines the key monitoring activities, their frequency, and the primary output each one produces.

| Monitoring activity | Recommended frequency | Primary output |

|---|---|---|

| Transaction anomaly review | Continuous, automated | Real-time alerts for investigation |

| Override rate analysis | Monthly | Workflow tuning recommendations |

| Supplier re-verification | Annual or on change | Updated, confirmed payee records |

| Staff fraud awareness training | Biannual | Reduced susceptibility to social engineering |

| Policy and threshold review | Quarterly | Calibrated controls aligned to current fraud patterns |

Beyond the operational cadence, regulatory compliance shapes what you must measure. The UK’s APP reimbursement framework requires institutions to demonstrate active prevention efforts, not just reactive claims handling. Holistic fraud strategies must also account for customer vulnerability and consumer protection obligations, which means your monitoring program needs to flag not just suspicious transactions but also potentially vulnerable account holders.

Tracking override rates is particularly valuable. If 40% of users are bypassing a specific CoP warning, that warning is not working. Detailed logging and tiered outcomes allow you to identify exactly which controls are being ignored and retune them before a fraudster exploits the gap. Staying current on AI-driven fraud trends also helps teams anticipate new attack vectors before they become widespread.

Key takeaways

Effective APP fraud prevention requires layered controls, precise verification workflows, strict operational procedures, and continuous monitoring to stay ahead of evolving fraud tactics.

| Point | Details |

|---|---|

| Layered controls are non-negotiable | Combine CoP, MFA, dual approval, and transaction monitoring for a complete defense. |

| Warning fatigue undermines controls | Use risk-based, specific alert messages and log every override to tune your system. |

| Operational procedures close technical gaps | Prohibit email-only bank detail changes and segregate payment duties across roles. |

| Regulatory exposure is real | The UK APP reimbursement framework splits costs 50/50 between PSPs, making prevention a financial priority. |

| Continuous tuning is required | Review override rates, thresholds, and staff training at least quarterly to keep controls effective. |

The uncomfortable truth about push payment fraud controls

I have reviewed fraud prevention frameworks across a range of financial institutions, and the pattern I see most often is not a technology gap. It is a design gap. Organizations invest in CoP systems and transaction monitoring platforms, then deploy them with generic alert messages and no override tracking. The technology works. The workflow around it fails.

The institutions that actually reduce APP fraud losses treat their verification controls the way a good engineer treats a production system: they instrument everything, measure what breaks, and fix it on a regular cycle. They do not assume that deploying a control means the control is working.

The regulatory pressure from frameworks like the UK’s APP reimbursement rules is useful here. It forces institutions to demonstrate active prevention, which creates an incentive to measure outcomes rather than just check a deployment box. But the organizations that wait for regulatory pressure to drive improvement are always behind the fraud curve.

The other thing I would push back on is the tendency to treat employee training as a soft control. In my experience, a finance team that genuinely understands how invoice fraud and BEC attacks work catches more fraud attempts than any automated system. Humans are the last line of defense in APP fraud because the payment itself is authorized. The technology can flag risk. Only a trained human can refuse to proceed.

Fraudsignals covers the identity verification controls and banking fraud trends that matter most to institutions building these defenses. The analysis there goes deeper than policy summaries.

— Kevin

Stay ahead of APP fraud with Fraudsignals

Fraudsignals tracks the fraud tactics, regulatory changes, and technology controls that financial professionals need to protect their organizations. The site covers everything from biometric verification and AI-led risk scoring to the operational procedures that stop APP scams before they succeed. If you are building or refining a fraud prevention program, the latest fraud intelligence on Fraudsignals gives you the context to make better decisions faster. Explore the full library of analysis and stay current on the controls that actually work in practice.

FAQ

What is Authorized Push Payment fraud?

Authorized Push Payment (APP) fraud occurs when a victim is deceived into willingly transferring funds to a fraudster-controlled account. Unlike card fraud, the victim authorizes the payment, which makes recovery difficult.

What does Confirmation of Payee actually do?

Confirmation of Payee checks whether the account name provided by the payer matches the name registered to the destination account. It returns a match, close match, or no match result, giving the payer a chance to cancel before funds are sent.

How does dual approval reduce push payment fraud risk?

Dual approval requires a second authorized person to confirm any payment above a set threshold. This prevents a single compromised or deceived employee from completing a fraudulent transfer without detection.

Why is warning fatigue a problem for fraud prevention?

When alerts are too frequent or too vague, users learn to dismiss them without reading. This means a genuine fraud warning gets bypassed at the critical moment, making the control ineffective regardless of how well the underlying system works.

What should businesses do immediately after suspecting an APP fraud attempt?

Contact your bank immediately to request a payment recall, document all communication related to the suspicious instruction, and follow your written incident response plan to escalate internally and preserve evidence.

Recommended

5 Signs Your Identity Verification Stack Was Built for 2019, Not 2026

The IDV market moved fast between 2019 and today. Document verification got more sophisticated. Liveness detection matured. Biometric binding became a realistic expectation rather than a high-assurance edge case. Fraud techniques evolved in parallel—and in some areas, faster.

If your